Press release 6.3.2026

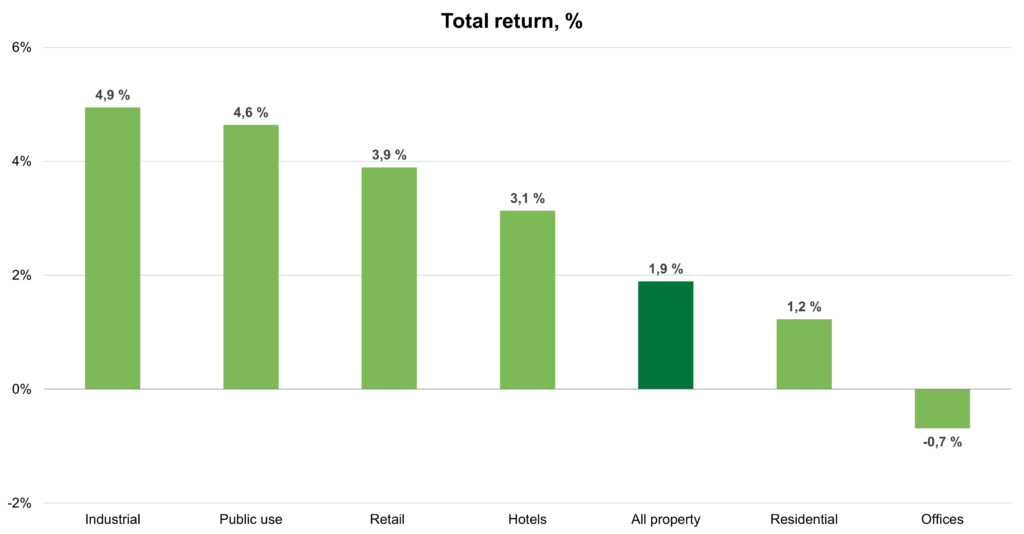

The total return on property investments held by professional investors increased to its highest level since 2021 and amounted to 3.5 per cent in 2025. Capital growth remained negative, however, the decline in capital values slowed down significantly compared to the previous three years. The average income return increased to 5.1 per cent, supported by both improved economic occupancy rates and lower capital values. Across the main property sectors, industrial properties delivered the highest total returns in 2025.

The KTI Property Index is based on 50 professionally managed real estate portfolios with an aggregate capital value exceeding € 35 billion. The index covers approximately 36 per cent of the professionally owned investment property universe. The KTI Property Index measures annual total return on standing investments, comprising annual realised net income and capital growth.

Capital values declined by 1.6 per cent on average

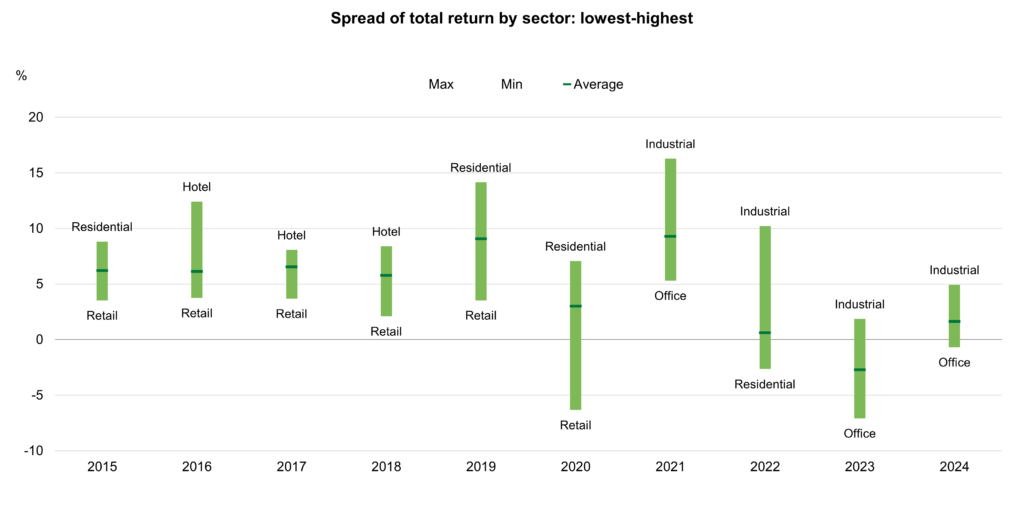

The increase in interest rates triggered a decline in the capital values of investment properties in 2022. In 2025, capital values continued to decrease, although significantly less than in the previous three years. The increase in yields continued to pressure capital values in 2025, however, towards the end of the year, yields started to stabilise as transaction activity in the property market picked up. Differences in total returns between property sectors remain pronounced. The average income return increased from 4.8 per cent in 2024 to 5.1 per cent in 2025.

Total return on residential properties increased to 3.3 per cent

Residential properties represent the largest sector of the professionally managed real estate investment market, accounting for approximately 35 per cent of the total invested universe. Capital values for residential assets declined sharply between 2022 and 2024, but in 2025, capital growth ended up only slightly in negative territory. The income return on residential properties continued to strengthen, primarily supported by lower capital values, but economic occupancy rate also improved compared to the previous year, averaging 93.5 per cent in 2025. The decline in capital values remained most pronounced within the newer residential stock. Among Finland’s major cities, capital growth turned slightly positive in Helsinki and Tampere.

Office properties remained the weakest performing property sector

Total return on office properties returned only marginally into positive territory in 2025, reaching 0.4 per cent, as the sector continued to be weighed down by uncertainty and weakening occupier demand. The average annual decline in capital values of office properties over the past five years has approached 5 per cent. In 2025, capital values were primarily pressured by a continued increase in yields, which rose more sharply for office assets than for other property sectors. Income return increased compared to the previous year, driven, however, solely by declining capital values, rather than underlying income growth. Economic occupancy rate in the office sector continued to deteriorate, falling below 80 per cent across the office portfolios covered by the Property Index.

Industrial properties delivered the best returns in 2025

Industrial properties – including warehouse, logistics and manufacturing assets – achieved a total return of 7.2 per cent in 2025. Over the past five years, industrial properties have been the strongest performing property sector, generating an average annual total return of 7.9 per cent. In 2025, industrial properties were the only sector to record positive capital growth. Returns were further supported by a significantly higher income return compared to other property sectors. Industrial properties, however, represent well below 10 per cent of the total value of the invested property universe in Finland.

Total return on retail properties increased to 4.8 per cent

The average total return on retail properties increased by nearly one percentage point compared with the previous year. Capital values continued to decline, although at a slower pace than in earlier years. Shopping centre assets underperformed other retail properties in 2025, as both capital growth and income return remained weaker than for other types of retail properties.

Capital growth of public use properties close to zero

The share of public use properties – assets used for the provision of publicly funded services – increased to over 10 per cent of the total property investment market in 2025. In recent years, the sector has demonstrated stronger performance than most other property segments. The sector’s returns are supported by stable income returns and high occupancy levels. Capital growth was only marginally negative in 2025, as yields remained broadly stable, and total return increased to 6.2 per cent. Among public use property sub-sectors, educational properties once again delivered the strongest performance, with capital growth turning clearly positive.

For more information:

Hanna Kaleva

hanna.kaleva@kti.fi

Managing director, KTI

KTI is an independent market information and research service company servicing the professional property investment sector in Finland.