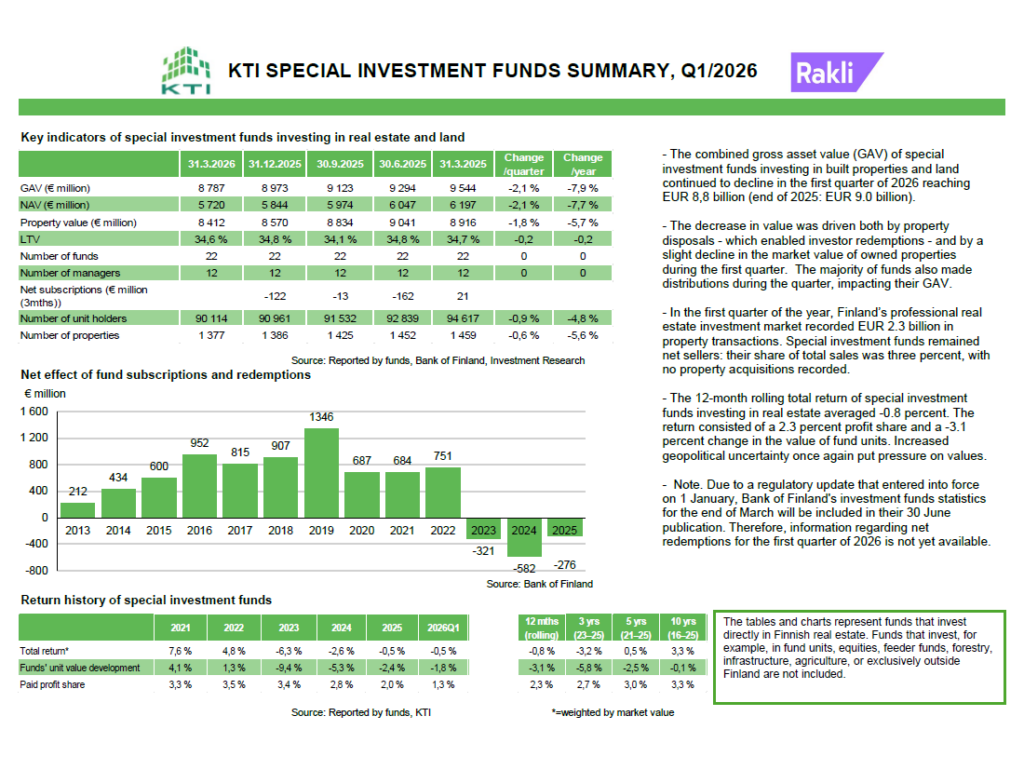

The Finnish Property Market 2026 report has been published.

Order The Finnish Property Market full report from here (free of charge).

Orders for printed reports and other matters, please contact us at kti@kti.fi or tel. +358 20 7430 130.

———————————————————-

The Finnish Property Market 2026:

Foreign investors continued to increase their investments in Finland in 2025

After more than two quiet years, the Finnish property market activity started to recover towards the end of 2025, and the annual transaction volume almost doubled from the previous year. However, property development volumes remained low in both residential and commercial property markets. In the rental markets, differences between property sectors and submarkets remain significant.

Economic development remained sluggish, and the Finnish GDP growth was estimated to be close to zero in 2025. Global geopolitical uncertainty, increasing unemployment and weak consumer confidence pressured private consumption, which continued to decrease slightly. Consumers’ weak confidence was, in many ways, also reflected in the housing markets, where both prices and rents continued to decline. Forecasts for GDP growth for 2026 are more positive at approximately 1%, as all components of the economy are expected to show positive development.

The size of the property investment market amounts to almost €97 billion

The total size of the Finnish invested property market amounted to €96.8 billion at the end of 2025, slightly up from the previous year. Market values of property investments continued to decline, but at a slower pace than in the two previous years, and investments in both new development and existing property stock compensated the negative capital growth. Foreign investors continued to further strengthen their role in the investment market and their share increased to almost 38% of the total market, which makes Finland one of the most internationalised property markets globally. In almost all domestic investor groups, the total amount of property holdings decreased slightly.

Residential properties represent 35% of the total invested market

Residential properties remain the largest sector in the Finnish property market with a clear margin. The total value of rental residential properties owned by professional investors amounted to almost €34 billion at the end of 2025, which represents 35% of the total market. The attractiveness of the rental residential property investments is supported by the solid population growth in the largest cities and the decrease in the average household size. The share of office properties remained stable, but that of retail properties decreased slightly from the previous year, due to a decrease in market values, low volumes of new development, and also increased investments by the major occupiers. Public use properties continued to increase their significance, and their share of the total invested market increased to 11%.

Transaction volume amounted to €4.4 billion

The total annual transaction volume almost doubled compared to the previous year. The increase in volume was partly due to various structural arrangements of property companies and portfolios, the financial challenges of a couple of sellers, and the materialisation of a few long-pending transactions. The growth was supported by the increased activity of foreign investors, who increased their acquisitions 2.5 times compared to the previous year and accounted for 60% of the total volume. The majority of the foreign capital was originated from other Nordic countries. For the first time ever, public use properties were the most traded property sector, with a 30% share of the total transaction volume. Supported by some large portfolio deals, the transaction volume of residential properties amounted close to €1 billion.

In the first two months of 2026, the volume of residential transactions already exceeded that of the whole year 2025, due to two large portfolio disposals carried out by Finnish institutional investors in anticipation of the upcoming pension reform. Investment demand of retail properties increased markedly in 2025, which resulted as the highest share of the total volume since 2018.

Total return increased to 3.5%

According to the KTI Property Index, Finnish property investments produced a total return of 3.5% in 2025, up from 1.9% in the previous year. Total return continued to be pressured by negative capital growth of -1.6%, but income return continued to increase and stood at 5.1% for all properties on average. The increase in yields was the main driver for negative capital growth, but towards the end of the year, yields started to stabilise. Industrial was, again, the best performing sector and produced a total return of 7.2%, supported by positive capital growth and a healthy income return. Public use and retail properties also continued to perform better than average. Total return of residential properties improved from the previous year and ended at 3.3%. After two years of negative total returns, office properties also returned to positive territory, with a total return of 0.4%.

Positive rental outlook for residential and industrial properties

Oversupply and the sluggish development of the economy have kept residential rental growth moderate or even negative in the Helsinki metropolitan area in recent years. In 2025, residential rents decreased by 0.9% in the metropolitan area on average. The occupancy rate, however, improved during 2025 and stood at 93.4% in December, which, together with the increasing population, low development volumes and strengthening economic development supports the stable or slightly positive outlook for rents. New rental residential development is currently focused on state-subsidised supply. Even in this segment, the volumes are expected to decline in 2026.

In the office markets, the KTI Rental Index for the Helsinki CBD decreased by 2.6% in 2025, as occupiers’ space needs continued to decline due to both hybrid work and increasing unemployment. Office vacancy rates in the main office areas in the Helsinki metropolitan area hit new records and stood at 18% on average at the end of the year. Also in the Helsinki CBD, the share of vacant office premises exceeded 18% in 2025. In the retail markets, rents remain stable and occupancy rates healthy. In the industrial space markets, the outlook remains more positive than in other commercial property markets.